Understanding your paycheck stub and implementing effective tax planning strategies are essential for managing your finances and maximizing your take-home pay. This article will delve into the significance of your paycheck stub and provide insights into various tax planning strategies to help you optimize your tax situation.

If you are seeking extra ways to fill and submit your financial documents without any hassle, here is paystubs creator from PayStubCreator that can ease all the processes.

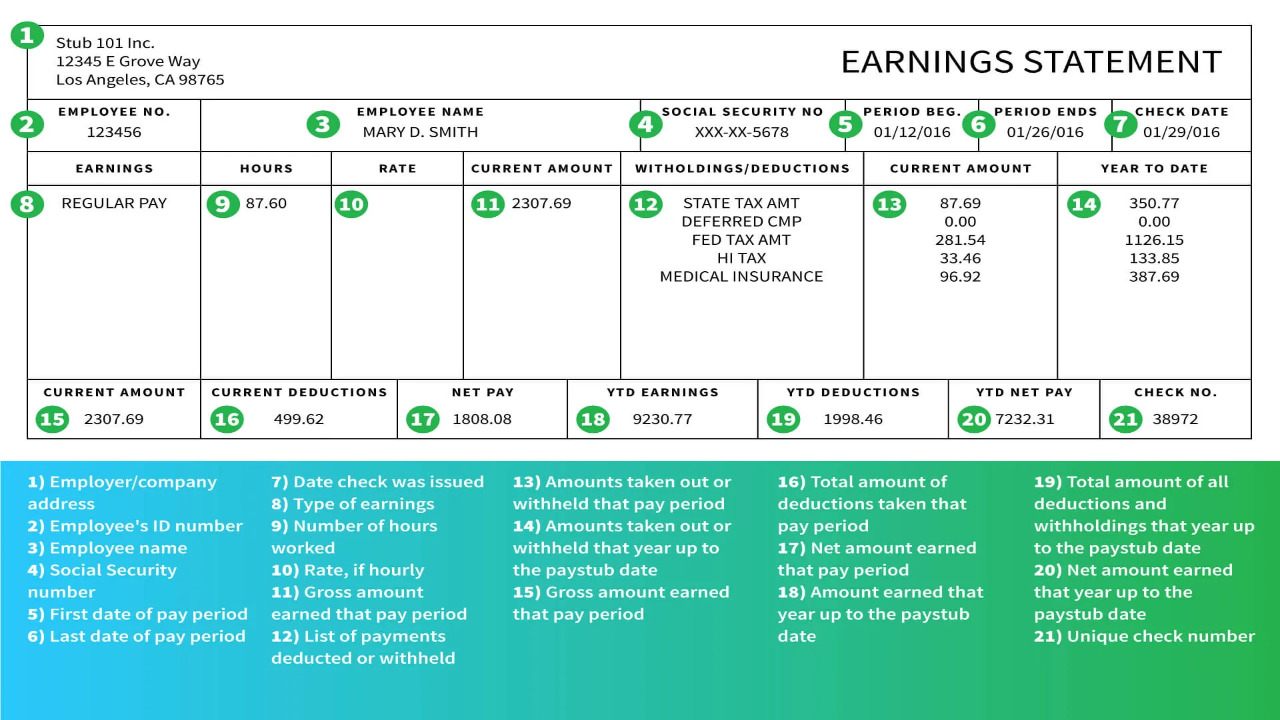

Understanding Your Paycheck Stub

Gross Income

Your gross income is the total amount of money you earn before any deductions, including taxes and other withholdings. It encompasses your salary, hourly wages, tips, commissions, and any other sources of income.

Taxes and Withholdings

Your paycheck stub will display various taxes and withholdings deducted from your gross income. These may include federal income tax, state income tax, Social Security tax, Medicare tax, and any other applicable local taxes. It is crucial to understand the different tax rates and brackets that apply to your income level.

Deductions and Contributions

Your paycheck stub will also outline deductions and contributions you have elected to make. These may include pre-tax deductions such as retirement contributions, health insurance premiums, flexible spending accounts, and other benefits. These deductions reduce your taxable income, thereby potentially lowering your overall tax liability.

Net Pay

The net pay, also known as take-home pay, is the amount you receive after all the deductions, taxes, and withholdings are subtracted from your gross income. It represents the actual amount you receive in your bank account.

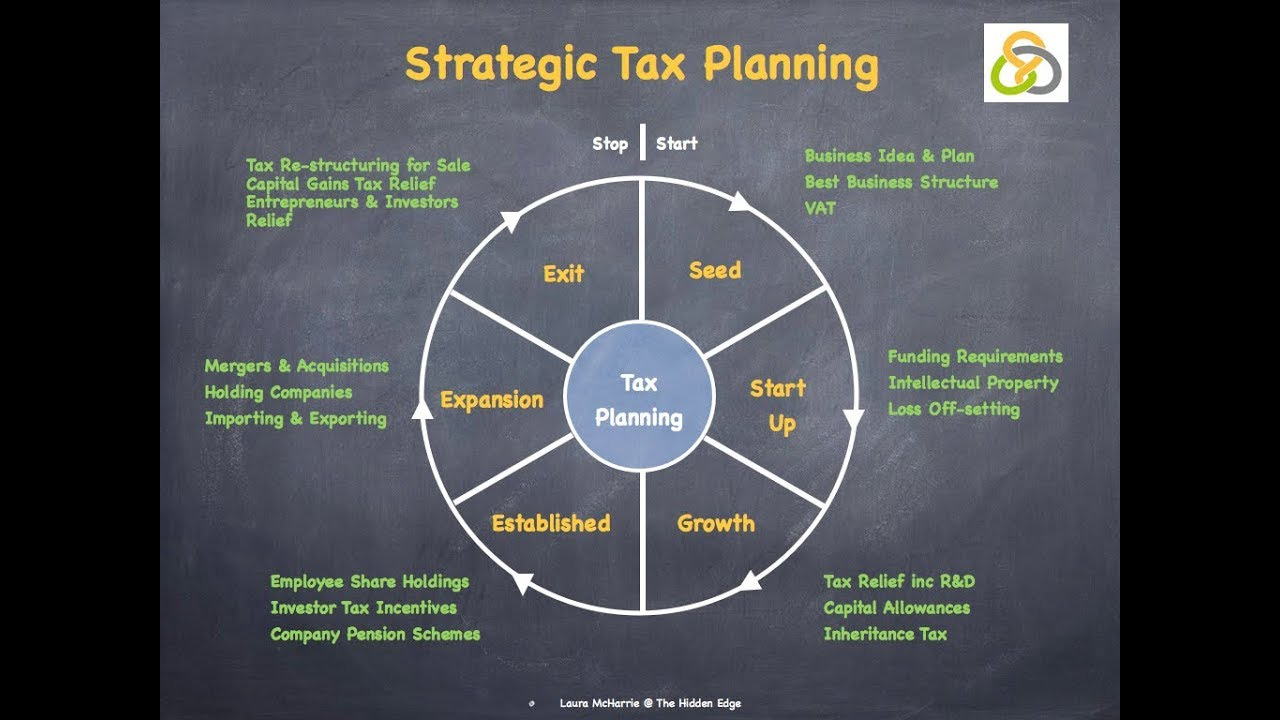

Tax Planning Strategies

Review Tax Laws and Updates

Tax laws and regulations change regularly. Staying informed about any updates or revisions can help you plan ahead and make adjustments to minimize your tax liability. Consult a tax professional or keep track of reliable sources to understand any new deductions, credits, or changes in tax rates that may impact your tax planning strategies.

Maximize Retirement Contributions

Contributing to retirement accounts such as a 401(k) or an IRA can provide immediate tax benefits. These contributions are typically tax-deductible, which reduces your taxable income. By maximizing your retirement contributions, you not only save for the future but also potentially decrease your tax burden.

Utilize Tax-Advantaged Accounts

Take advantage of tax-advantaged accounts, such as Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs). HSAs offer tax benefits for medical expenses, while FSAs allow pre-tax contributions for qualified healthcare expenses. Utilizing these accounts can help you reduce your taxable income and save on medical costs.

Consider Itemizing Deductions

If your eligible deductions exceed the standard deduction, consider itemizing deductions on your tax return. Common itemized deductions include mortgage interest, state and local taxes, charitable contributions, and medical expenses. By carefully tracking and documenting your expenses, you may be able to reduce your taxable income further.

Plan Capital Gains and Losses

If you have investments, strategically planning your capital gains and losses can be advantageous. Consider holding investments for more than a year to qualify for long-term capital gains rates, which are typically lower than short-term rates. Additionally, offsetting capital gains with capital losses can help minimize your overall tax liability.

Understanding your paycheck stub and implementing effective tax planning strategies are vital for managing your finances and optimizing your tax situation. By familiarizing yourself with the components of your paycheck stub, staying updated on tax laws, maximizing deductions and contributions, and planning your investments wisely, you can reduce your tax burden and make the most of your hard-earned income. Consider consulting a tax professional to tailor these strategies to your specific financial circumstances and goals.